It’s a straightforward calculation — multiplying the current stock price by the total number of outstanding shares. To sum it up, a weighted average of a company’s outstanding shares gives a more accurate picture of how much a company earned for its investors over a specified time period. It takes into account changes in the company’s outstanding shares over time and better reflects how much profit the company produced per share. When a company calculates its earnings over a certain period of time, it divides its profits by the number of outstanding shares. However, companies‘ outstanding shares can change over time as a result of newly issued shares, repurchased shares, exercised employee stock options, or several other reasons. Your broker can help you sort out the details — head on over to our Broker Center if you’re looking to get started investing.

Outstanding Shares

These shares are non-dilutive because they do not include any options or securities that can be converted. The weighted average number of shares outstanding means the equivalent number of whole shares that remain outstanding during a particular period. It is computed by multiplying the number of common shares by the fraction of the period they have been outstanding. Understanding the gaap consistency principle: how it affects your business the difference between weighted average shares and shares outstanding is vital if an investor is to build a portfolio that will perform according to their expectations. These two calculations provide information on how well a company performs over time. If a company considers its stock to be undervalued, it has the option to institute a repurchase program.

Part 2: Your Current Nest Egg

These include changes that take place because of stock splits and reverse stock splits. There are also considerations to a company’s outstanding shares if they’re blue chips. The weighted average of shares outstanding is used to determine a publicly-held company’s earnings per share. Privately-held companies are not required to report earnings per share, so they do not need to calculate this number. A stock split increases the number of outstanding shares but requires adjusting WASO to ensure comparability across reporting periods, as the company’s value doesn’t change. The total number of shares outstanding directly influences a company’s market capitalization, essentially indicating its total market value.

Outstanding Shares and Share Repurchase Programs

A company may announce a stock split to increase the affordability of its shares and grow the number of investors. For instance, a 2-for-1 stock split reduces the price of the stock by 50%, but also increases the number of shares outstanding by 2x. The following are the three steps to calculate weighted average shares outstanding.

- The number of shares outstanding can change substantially over the course of a year.

- Consequently, the treatment of stock dividends and splits is different from the treatment used for issuances of shares in exchange for assets or services.

- Corporations issue shares to raise capital, and the number of shares that have been bought and are currently owned by all shareholders is known as shares outstanding.

- The number of shares outstanding increases whenever a company undertakes a stock split.

- Outstanding shares include share blocks held by institutional investors and restricted shares owned by the company’s officers and insiders.

In above example, notice that Maria Company has adjusted all shares that exist prior to stock dividend (i.e., from January 1 to June 1). The purpose of this adjustment is to state these shares on the same basis as shares issued after the date of stock divided. The shares issued after stock dividend have not been restated because these shares have been issued on new basis and require no adjustment. A stock dividend only affects those shares that already exist prior to its occurrence.

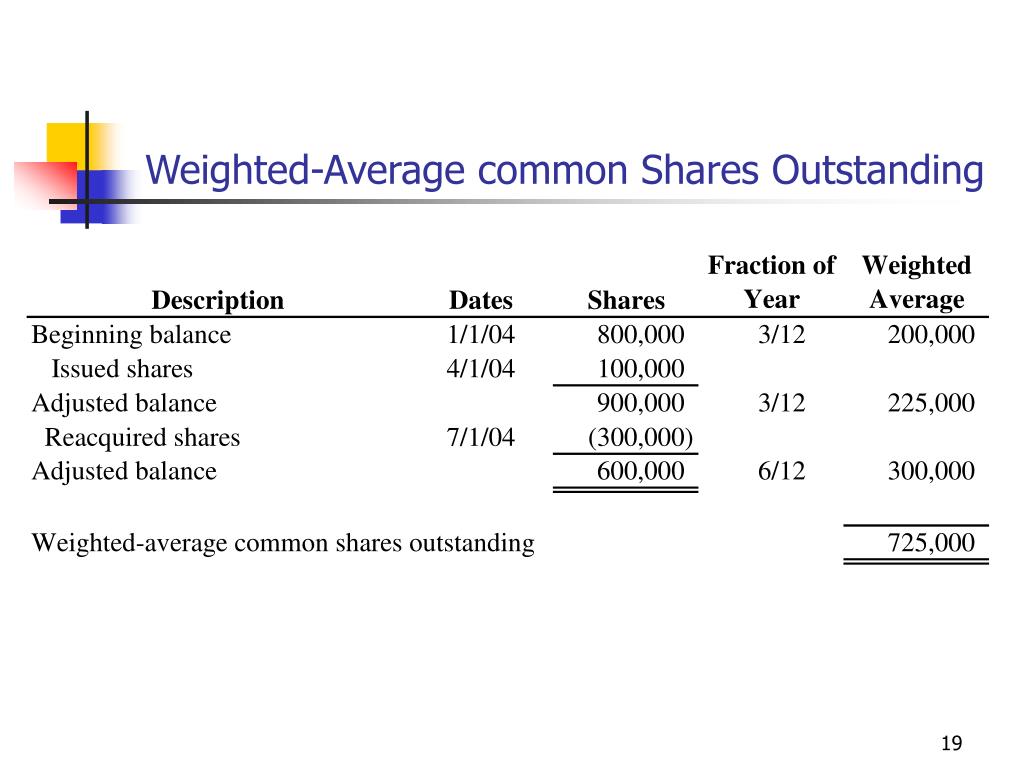

Certain corporate actions, like stock splits, share issuances, or buybacks, necessitate adjustments in the WASO calculation. Suppose that Sample Company had 100,000 shares of common stock outstanding on 1 January 2021, that 20,000 shares were issued for cash on April 1, 2021, and that 12,000 shares were retired on 1 September 2021. Different scenarios for calculating the weighted average of outstanding shares are shown in the following examples. Consequently, the treatment of stock dividends and splits is different from the treatment used for issuances of shares in exchange for assets or services. Let us see how the weighted average number of shares outstanding will change.

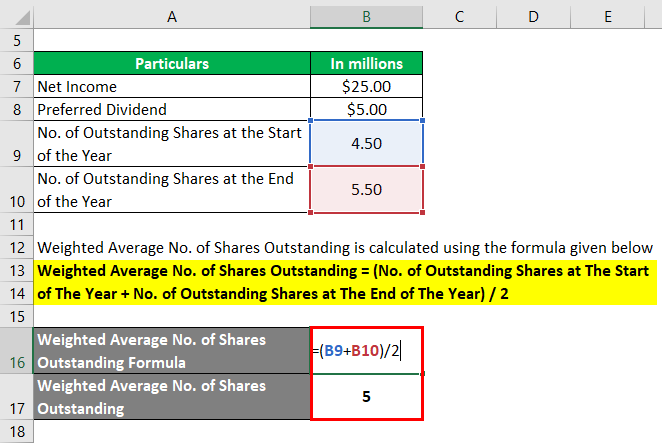

Before delving into the weighted average aspect, it’s essential to grasp what shares outstanding represent. Corporations issue shares to raise capital, and the number of shares that have been bought and are currently owned by all shareholders is known as shares outstanding. Weighted average shares outstanding is the process of weighting every number of common stock to reflect how much time they were in effect. When the number of outstanding shares is changed by a stock dividend or split, the firm’s earning power is not affected. To calculate this weighted average, first input the two values for the number of shares outstanding into adjacent cells. In our example, during January, there were 150,000 shares, so this value is entered into cell B2.

The trajectory of WASO over time can signal a company’s strategy and financial health. A consistently rising WASO might indicate a company’s reliance on issuing new shares for funding, possibly diluting existing shareholders’ value. Start by segmenting the reporting period into intervals where the number of outstanding shares remained constant. The shares can be grouped according to the length of time that they were outstanding. In this case, group 1 consists of 100,000 shares that were outstanding for the entire year, while groups 2 and 3 are included in the 20,000 shares issued on 1 April.

While the lower number of outstanding shares often hampers liquidity, it could also deter short sellers since it becomes more difficult to borrow shares for short sales. Using weighted average shares outstanding gives a more accurate picture of the impact of per-share measurements like earnings per share (EPS). Note that this method does not account for shares that can be potentially released through various mechanisms, so a weighted average shares outstanding will not tell you the diluted EPS. A stock split, for example, increases the number of shares but does not change the company’s market capitalization.

We have seen corporate actions above and their treatment of the weighted average outstanding shares. If the Company buys back the shares, they are treated similarly to the shares issued, but on the opposite, the shares are reduced from the calculation. Let’s say that a company earned $100,000 this year and wants to calculate its earnings per share (EPS). At the beginning of the year, the company has 100,000 shares outstanding but issues an additional 50,000 halfway through the year, for an ending total of 150,000. Instead of computing EPS based on the ending number of shares, which would produce EPS of $0.67, a weighted average should be taken.

And finally, the business might issue shares to the owners of a business that it is acquiring. In a larger corporation, these factors can result in substantial ongoing changes in the number of shares outstanding, making it more difficult to calculate the weighted average of shares outstanding. Dilution occurs when a company issues additional shares, reducing current investors‘ proportional ownership in the company. The weighted average of outstanding shares is a calculation that incorporates any changes in the number of a company’s outstanding shares over a reporting period.